Related Topics

No topics are associated with this blog

The Disaster of Negative Rates

“There is no barrier for U.S. Treasury yields going below zero. Zero has no meaning, besides being a certain level.”

–Former Fed Chair ALAN GREENSPAN in August 2019

“I am not a fan of low interest rates, as a great believer in the importance of savings in the economy. Subsidies to debtors and penalties for savers, I think in the long term harms the economy.”

–Credit Suisse CEO TIDJANE THIAM

“It is hard to imagine a more stupid or dangerous way of making decisions than by putting those decisions in the hands of people who pay no price for being wrong.”

–DR. THOMAS SOWELL, former Forbes columnist and acclaimed author

______________________________________________________________________________________________________

INTRODUCTION

For over 30 years, I have read every Barron’s Roundtable edition interviewing many of the world’s foremost money managers. Past and current members have included Peter Lynch, Mario Gabelli (still a participant), Bill Gross and, though not nearly as well known, one of the best stock pickers extant, Meryl Witmer. Accordingly, it was with great pleasure that I discovered a former member of the esteemed cohort is also an EVA reader.

He had emailed me about our “A Blast From A Bubble Past” EVA back in June that discussed the raging mania in the IPO (Initial Public Offering) market. He was most complimentary about that chapter of our “Bubble 3.0” series and he particularly enjoyed the vignette about our tennis ball-swallowing dog who turned up his big, wet nose at a Beyond Meat burger patty.

Then, in July, I asked him what he thought about the next chapter, “The Post Retirement Society” and especially my rant against the bizarre phenomenon of negative-yielding bonds. While his comments were generally positive, he did make a case that bonds an investor has to pay to hold aren’t totally deranged. His point was that if enough people are really worried about another monstrous deflationary bust along the lines of 2008, then it isn’t completely illogical to pay the German government a small amount each year to hold a genuinely risk-free security. He’s far from alone.

On that score, do you know what the fastest growing asset class is this year? That would be bonds with negative yields. In fact, 30% of the planet’s securities now “sport” negative interest rates. Further, with each passing week there seems to be another trillion added to the total which now amounts to around $17 trillion. As a result, 95% of the planet’s investment grade bond yields are made in America. Essentially, the rest of the world has gone yield-free, at least on high-quality debt. And this is before the upcoming grand finale by European Central Bank chief Mario Draghi next month. Mr. Draghi, who is stepping down at the end of this year, has made it disturbingly abundantly clear that he intends to go out with a big bang of monetary pyrotechnics. This has the very real potential of forcing eurozone yields even deeper into the red.

This week’s edition of our Guest EVA is, once again, courtesy of my long-time friend and investment newsletter legend John Mauldin. As many EVA readers are aware, his weekly “Thoughts from the Frontline” is free and yet it frequently contains financial insights every bit as profound as those available from high-cost sources. (You can subscribe via this link.) John also does his own version of a guest newsletter which he calls “Over My Shoulder”. His most recent, written by Thorsten Polleit of the Mises Institute, is dedicated to what the author refers to as “The Disaster of Negative Interest Policy”.

As he points out, one of the reasons why negative yields have been spreading like a highly contagious virus on a cruise ship is that they allow debt-addicted governments to finance their enormous obligations at either basically zero or, astoundingly, sub-zero. As he writes, “running into debt becomes a profitable business, and financially ailing states and banks can reduce their debt burden at the expense of creditors”.

In Denmark today, it is possible to take out a mortgage that pays the borrower each month! As Mr. Polleit also notes: “If anyone can suddenly get a loan with a negative interest rate, then it is to be expected that credit demand will get out of hand.” And a bit later: “The low interest rate policy facilitates a spectacular inflation of prices in the asset markets; a gigantic speculation bubble is pumped up.” One certainly doesn’t have to look any further than the crypto currencies or new-issue US stocks to witness this effect.

He also astutely articulates the deleterious impact negative yields have on savings and investment decisions. As these pages have frequently observed, hundreds of millions of Baby Boomers worldwide are waking up to the terrifying reality of not being able to earn an adequate return on their portfolios. This causes them to spend less and save more – an economic irony John Maynard Keynes coined as the Paradox of Thrift – which is pretty much the opposite of what the central banks are trying to achieve.

As always, there are winners and losers from misguided policies. A glittering star this year has been gold which is now up 20% and gold mining stocks are up an even more impressive 42%. It wasn’t long ago the miners were even more out of favor than energy issues are now. Evergreen was one of the few touting them at the start of the year as beneficiaries of negative yields. US bonds, of course, have also produced outstanding gains this year with the 10-year T-note having posted a total return of 11.5%.

Yet, frankly, the list of losers is considerably longer, particularly once artificially inflated asset prices begin to crack, as many have started to do. Moreover, the truly “Fearmaggedon” scenario would be a global recession with central banks already in max stimulus mode—and then some. Not to worry, though; according to Ned Davis Research the probability of a global recession is only 96%. Now, don’t you feel better?

______________________________________________________________________________________________________

THE DISASTER OF NEGATIVE INTEREST POLICY

By Thorsten Polleit

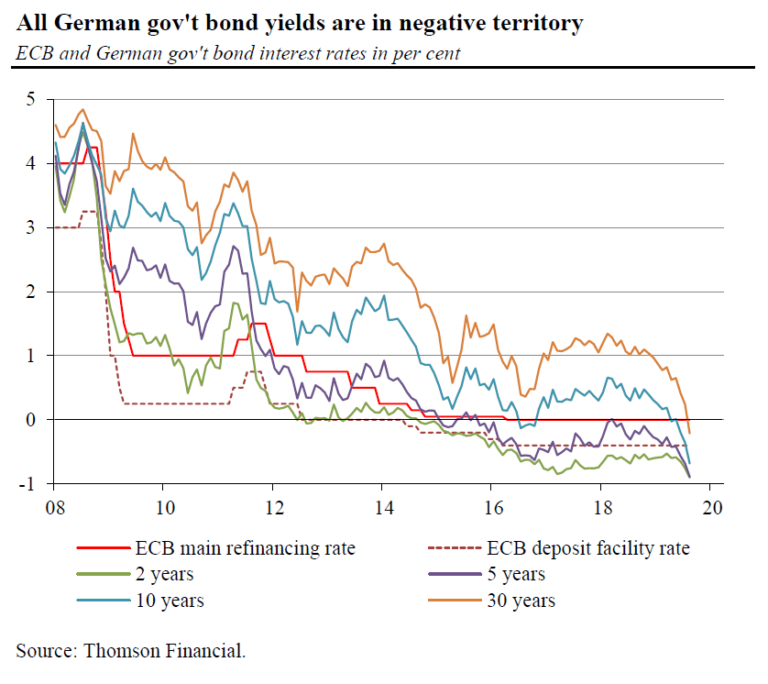

Those who had hoped that things could not get worse with the monetary policy of the European Central Bank (ECB) have been proven wrong. At its last meeting on 25 July 2019, the Governing Council of the ECB kept interest rates unchanged: the main refinancing rate was kept at 0.00% and the deposit rate at -0.40%. At the same time, however, ECB President Mario Draghi has prepared the ground to lower interest rates even further in the coming months. What is the reasoning behind that?

According to the ECB Governing Council, inflation is too low, and the euro area economy is too weak. It was precisely this assessment that signaled to the markets to expect a rate cut in the near future. It has now become very likely that the deposit rate will be lowered by 0.2 percentage points to -0.60% at the next ECB meeting in September; and the main refinancing rate could drop to -0.20%. The continued path into the negative interest world, however, has quite dramatic consequences.

The Essence of the Interest Rate

This becomes clear when considering what the interest rate stands for. In short, it represents the value discount that a later satisfaction of a want suffers compared to an earlier satisfaction of the same want (under otherwise identical circumstances). The “pure” or “originary” interest rate is positive — always and everywhere. It cannot disappear, it cannot go to zero, let alone fall below the zero line; the logic of human action informs us that the pure interest rate cannot be thought away from human actions and values.

However, there is the “new negative interest rate theory,” saying that the “new natural interest rate” — or: the “social pure interest rate” — has become negative. And while this theory is wrong, it has already found its way into monetary policymaking; presumably because it is highly attractive to the state and those groups closely associated with it because if the central bank forces interest rates into negative territory, running into debt becomes a profitable business, and financially ailing states and banks can reduce their debt burden at the expense of creditors.

The fact that many market interest rates in the euro area are now in the negative range is by no means an evidence of the validity of the “negative interest rate theory.” Market interest rates are manipulated to the core. They are dictated by central banks — and not just the short-term, but also the long-term interest rates: The monetary authorities buy debt securities, thereby increasing their prices and lowering their returns. That is why many interest rates have become negative; it is not a “natural” development; it has been orchestrated by the ECB.

Negative Interest for All

Is it conceivable that in the euro area consumer-, home construction-, and corporate loans will soon be offered at a negative interest rate? Yes, it is possible, indeed. To illustrate how this could occur, we assume that euro commercial banks get credit from the ECB for minus 2% per annum: Banks borrow 100 euros, and after one year, they pay 98 euros back. So the banks easily reap a profit of 2 euros. However, the ECB will let the banks only borrow at negative interest rates under the condition that they lend the money.

To stick with our example: A bank borrows 100 euro for one year at minus 2% per year from the ECB. It lends the money to consumers at, say, minus 1% (giving them €100 and getting €99 back after one year). Overall, the bank makes a profit of 1 euro: It earns 2 euros by borrowing from the ECB while losing 1 euro in the lending business. A twisted world, and it does not bode well for the prosperity of the economies.

The Way into the Planned Economy

If anyone can suddenly get a loan with a negative interest rate, then it is to be expected that the credit demand will get out of hand. To prevent this from happening, the ECB will have to resort to credit rationing: It determines in advance how many new loans it wishes to hand out, and then allocates this amount of credit. The credit market no longer decides who gets what and when and on what terms and conditions; those decisions are made by the ECB.

According to which criteria should loans be allocated? Should anyone who asks for credit get something? Should employment-intensive economic sectors be favored? Should the new loans only go to ‘the industries of the future’? Should weakening industries be supported with additional credit? Or should Southern Europe get more than Northern Europe? These questions already indicate that the planned economy is established through a policy of negative interest rates.

More than ever it will be the ECB that reigns over credit: It will effectively determine what will be financed and produced and where and when; it will determine who will be in a position to buy and consume on credit. As a central planning authority, the ECB — or the groups that greatly influence its decisions — determines everything: which industries will be promoted or suppressed; which economies are allowed to grow stronger than others; which national commercial banks are allowed to survive and which are not. Welcome to the planned economy in the Eurozone!

Speculative Bubbles

But that is not enough. The process toward ever lower interest rates drives asset price inflation: Stocks, houses, and land — everything becomes more expensive. Because the lower the interest rate, the higher the present value of future payments and thus the market prices of assets. The low interest rate policy facilitates a spectacular inflation of prices in the asset markets; a gigantic speculation bubble is pumped up.

This initially offers investors high returns. At the same time, however, the future yield prospects worsen. This can be explained as follows: Zero interest rates make investors bid up the prices of stocks and houses until the expected future returns of these assets are close to the zero interest rate set by the central bank. In the extreme case, when the central bank sets negative interest rates, expected market yields can even fall below zero.

Once central bank policy has succeeded in pushing all returns to or below zero, the free market economy is about to end. Without a positive return in sight, saving and investing stops: Because acting man has a positive originary interest rate, it no longer pays off to save and invest. The division of labor economics comes to a shrieking halt. Replacement and expansion investments will no longer take place. Capital consumption begins, and the modern economy falls back into a primitive subsistence economy.

The End of the Free Society

The monetary policy of zero and negative interest rates — if it is consistently thought through — leads to the demise of (what little is left of) the free society as we know it in the Western world. The destructive effects of a negative interest rate policy are not immediately obvious to most people, because the path toward negative interest rates may be accompanied by an artificial economic upturn that gives the impression that the economy looks good, even though it effectively lives off its substance.

Only gradually, the damage becomes visible. Economic growth is dwindling; political conflicts over income distribution are increasing; the state becomes more and more powerful; the degree of freedom for citizens and businesses decreases; and at some point, asset prices collapse and the bubble bursts as economic performance becomes increasingly impaired: Companies make less profit, jobs are lost, and consumers must rein in their demand.

All this leads to economic impoverishment and, most likely, eventually to political chaos. The negative interest rate policy proverbially cuts off the branch on which the welfare democracy of the Western world is sitting. The harmful consequences of a negative interest rate policy are already clearly visible today. If central banks are not prevented from pushing interest rates to zero or into negative territory, this will turn out to be one of the greatest tragedies of our time.

Originally published: Sunday, September 01, 2019; most-recently modified: Sunday, September 01, 2019