The Argument for Designating Obstetrical Cost, As a Cost of the Child.

It may seem strange we shifted obstetrical costs in our proposal from cost-to-mother, to cost-to-child, but here's why it was done. In the first place, it smooths out the huge cost of large families, into an identical cost per child. Persons who prefer small families may think this favors religious preferences, but its real motive was to create insurance neutrality for people in choosing the family size. If the consequence turns out to be families like my grandmother's with thirteen children (or Ben Franklin's with eleven), the formula could, and probably would, be adjusted. At the same time, it should be pointed out this shift allows insurance to overcome the present nearly insurmountable tendency of women to delay their first child until it becomes both a medical (Down's Syndrome for example) and social (male-female employment inequality) problem. There may be other ways to accomplish this goal, but I can't think of any.

The proposal, remember, is to begin employment insurance at age 25, and to make zero to age 24 health coverage into a gift from a designated grandparent's escrow account, paid out of the grandparent's surplus accumulated during a lifetime of his last-year-of-life re-insurance. The necessary assumption is that the Affordable Care Act can do as it pleases with insurance for a worker, just so long as it neither adds nor subtracts from the child's escrow fund, but lets the balance continue to grow its compounding investment income. This is the price asked from both the Affordable Care Act and employer-based insurance, in return for eliminating the expensive part of obstetrical costs from their cost obligations.

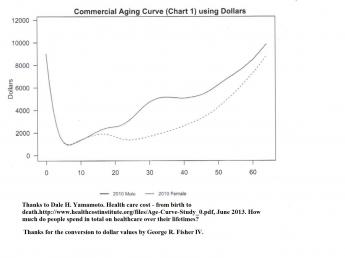

This clarification returns us to the medical cost curve derived from multiplying the average yearly weight provided by Dale H. Yamamoto by the lifetime dollar cost provided by insurance carriers. I must thank both these sources for their data, and my son, George IV, for performing the conversion. The resulting U-shaped curve is missing obstetrical cost from the first year of life, but largely contains it buried in the upward bulge in female costs from age 20-40. (To be fair, it also contains it in the low cost of male health insurance during the same period, if you believe family plans assume an equally-divided present responsibility between the two parents. That's the assumption we make when we draw a hypothetical line between the two during that interval. It makes no claim on precision, but for plan-design purposes, it is close enough. One must remember the way these calculations are made, results in omitting the insurance company overhead and profit. It also makes the cash payments for deductibles and copayments into an approximation. The resulting curve is in the planning ballpark, but must not be quoted as precise.

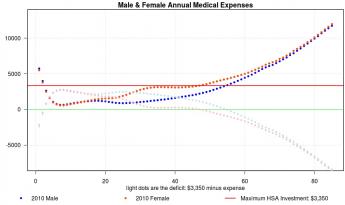

In the second graph, we dotted-in the two consequences, one of which shows the average woman probably could not afford to finance her retirement from HSA surplus, while the other shows it would become more comfortable by transferring away some obstetrical cost and compounding it. By itself, that fact is convincing this approach is a necessary one, but it may require legislative approval. For the time being, it remains the government's choice. For that combination of reasons, we offer first and last year of life re-insurance as a planning suggestion for discussion, rather than a proposal for immediate action.

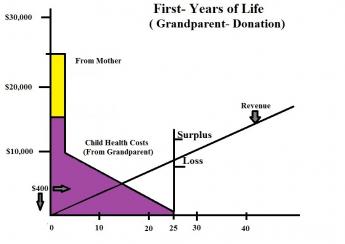

And in the third graph, we have presented a schematic of what we just said. It isn't very complicated in the schematic, but it may well be a little confusing to hear it described. Just in case it still isn't clear, the grandparent account pays all childbirth costs or about $18,000 for both childbirth and the first 25 years of the child. The mother is relieved of the childbirth part of her obstetrical costs as a gift from her parent, and this gift is paid for by compound interest. Things have mostly handled this way to keep them within the donor's account, thereby avoiding disputes about ownership. The grandparent is regarded as having earned this money and therefore controls how it is to be spent. He/she spends it this way in order to receive the last-year-of-life and retirement benefits as a consideration.

Originally published: Thursday, May 12, 2016; most-recently modified: Thursday, June 06, 2019